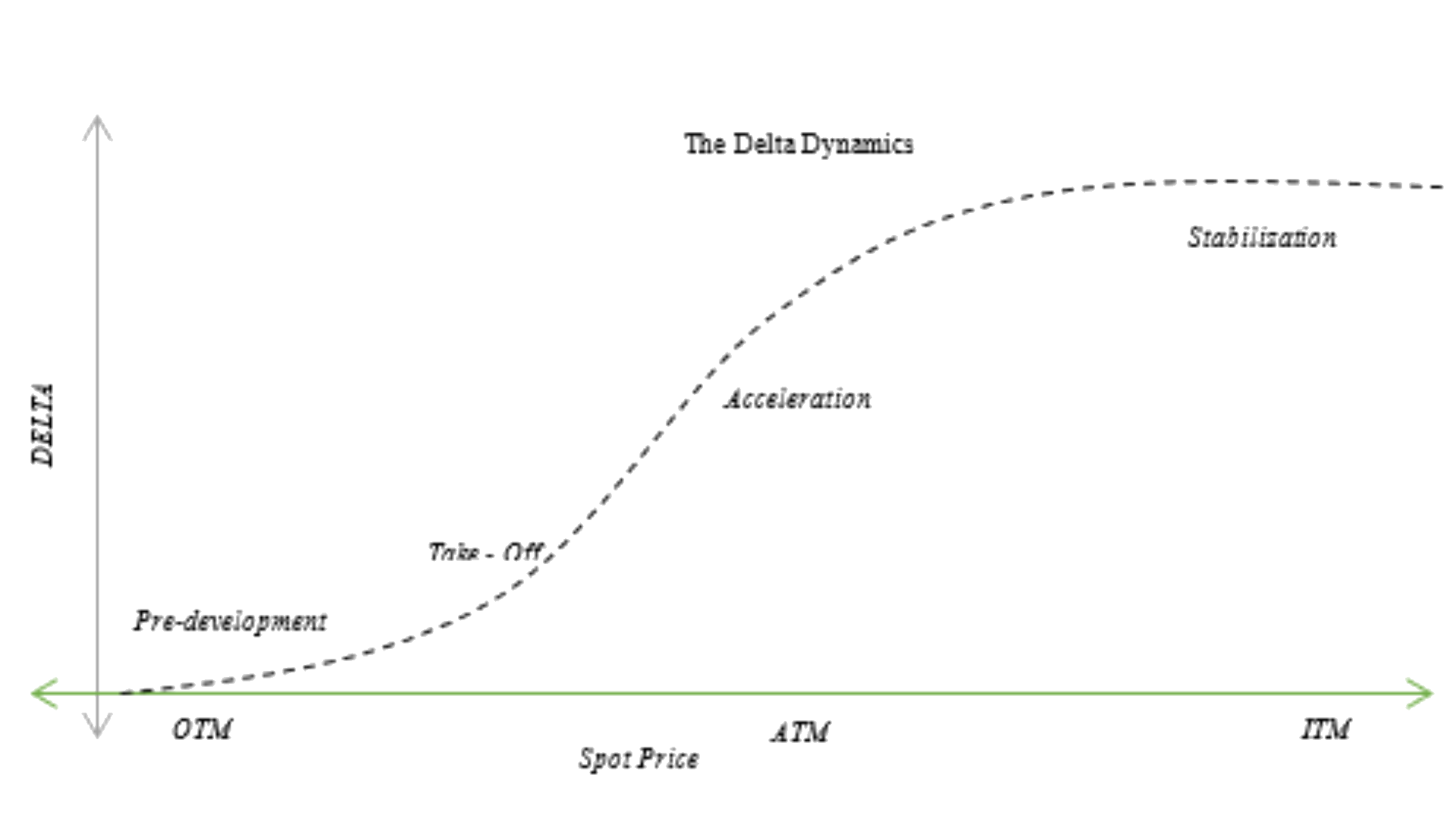

Option Delta, by definition, is a first order option Greek, measuring the sensitivity of option premium to the change in underlying price. If the option under consideration is an equity option, implies that the underlying is stocks, or NSE F&O segment stocks. On NSE, the F&O segment has equity indices, also, like Nifty/BankNifty/FinNifty. Nifty traders, can trade the index using options or futures, of which options are the preferred contracts. The basic knowledge of option trading isn’t sufficient for efficient option trades. The need to understand option greeks is extremely necessary.

As discussed, Option Delta, first-order option Greek, is change in option premium, due to directional price change in the underlying, keeping other factors same. So, for example, if option Greek, delta, is 0.68, implies that if the underlying directional change is +1, then the option premium shall increase by 0.68 in case of a call option, and drop by 0.68 in case of a put option.

An option delta of 1 means that the option price will move in lock-step with the underlying asset's price, while a delta of 0 means that the option price will not change with the underlying asset's price. As the put option (discussed in above example) reduces in price on increase in underlying price, the direction of the two price movements is opposite and option Greek, delta of the put option is therefore, negative. Delta can also be expressed as a percentage, with values ranging from 0 to 100 for call options and from 0 to -100 for put options.

Consider the example on option calculator of NIFTY option,

Nifty

Expiry: 25 Jan 2023

CMP: 18158

18200 CE: Rs 45

Observing the option chain, 18200 CE of Nifty, Delta is 0.4 implying if Nifty moves from 18158 to 18168, option should gain by Rs 4.00.

Also, a glance at the Nifty option chain suggests the Implied Volatility is 11.4%.